June 8-12, 2026

Roofers/Contractors/Homeowners/PIA/Staff/Independent

This is a simple, neutral roadmap for homeowners, insurance carriers, contractors, and anyone involved in a property claim (especially the recent Dallas/Fort Worth hail and storm damage).

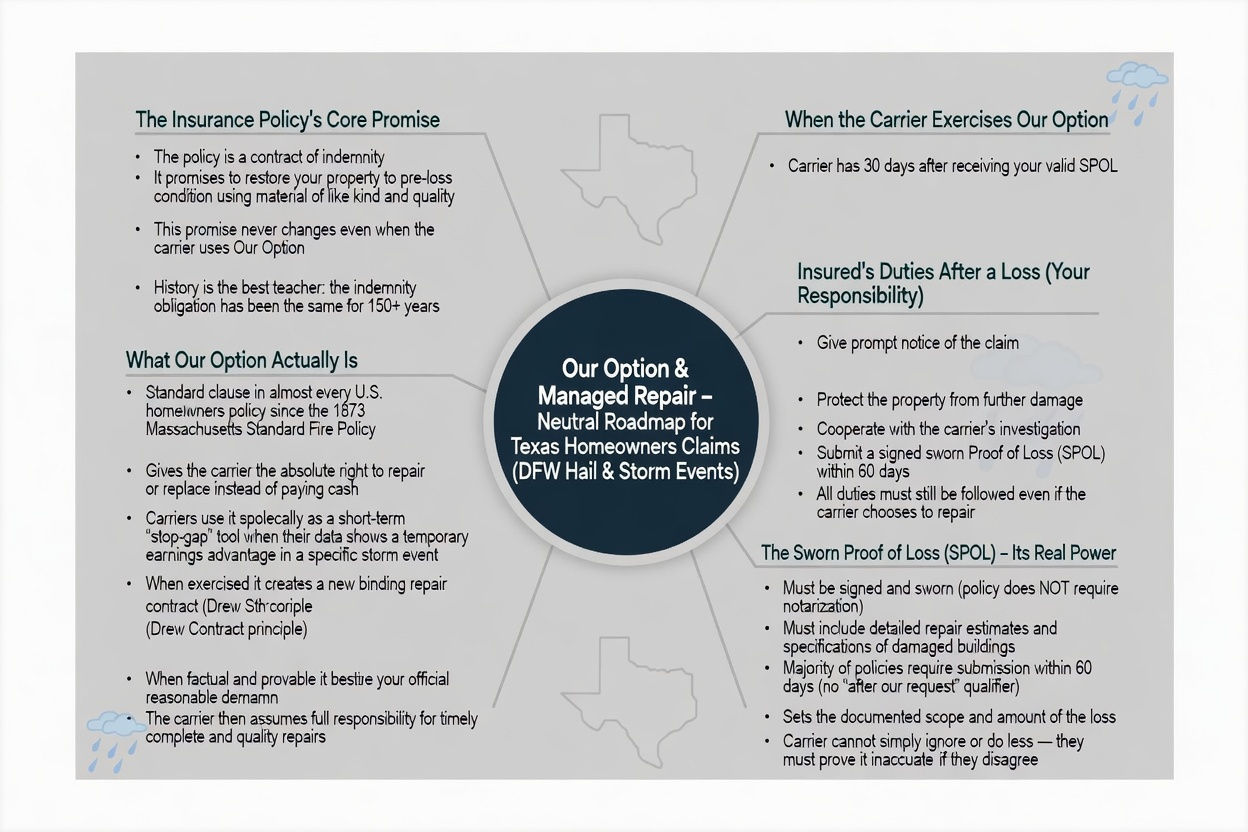

"Our Option" is a long-standing clause that appears in almost every standard homeowners policy in Texas and across the U.S. It gives the carrier the absolute right to choose to repair or replace the damaged property with material of like kind and quality instead of just writing a check. This right has existed for over 150 years and is clearly written into the policy. Carriers like Travelers and others are now exercising it more often after major storms. Nothing in this roadmap changes the carrier’s right to use “Our Option.” It also does not change the core promise of the policy: to put the insured back to pre-loss condition (the contract of indemnity).

The goal here is simply to explain, in plain English, what the policy actually says and what is supposed to happen step-by-step when everyone follows the rules.

Clear communication and proper documentation help the process go smoother for all three main parties — the insured (you, the homeowner), the carrier, and the contractor who may do the work.

(This ties directly into the Advanced Xact Field Training. First we teach you what is covered, then we teach you how it is covered, then we teach you how to transfer it to paper... Into what should become the insured's SPOL.)

The new classroom is located at 11037 Highway 6, Sante Fe, Texas 77510

Statute, POLICY, and the Facts of the Loss... These are three bullets that are necessary for ANY claim to find successful indemnification.

They are using it to find obscure exclusions, language... and conditions precedent... Precedent for what you may ask... for a denial.

We specifically teach how to find, read, comprehend... and APPLY those bullets for the most precise outcome, according to those facts.

Our course equips students to safeguard families’ futures by ensuring insurance claims deliver promised indemnity. For 150 years, well-funded, amoral insurers have crafted complex policies with hidden duties, like the Sworn Proof of Loss, inflicting a "death by a thousand cuts" process through high deductibles, reliance traps, and denials, as in Billie v. Plymouth Rock (2025). Learn to submit a detailed Proof of Loss to secure rightful payments. For contractors and adjusters, this training prevents financial ruin and defends every insured.

Bootcamp’s Counter to the Cuts

Our Public Adjuster Bootcamp, training Contractors, Independent Adjusters, Attorneys, and Staff Adjusters, prevents these cuts by:

- Providing a process to open and close a claim… within 90 days. Regardless of whether the insurance carrier chooses to participate, or not, at any level.

- Teaching submission of a Sworn/Notarized Proof of Loss with detailed estimates, avoiding Billie-like denials, with a court decision to back it up.

- Teaching the actual policy, how to read it, and the statutes that govern them, by an actual attorney who does it.

- Exposing amoral tactics, like notarization traps, by advising insureds to attach their own estimates as “Exhibit A,” restoring the 165-line policy’s intent for accessible compliance.

- How to file proper complaints, and why. Complaints are not a tool to entice a carrier to pay. They must be valid, violate the statute, and not be about coverage. The DOI is not a court; they are a regulatory body. They can and will act upon violations of the statute, i.e., popped timelines, etc. This is the core reason. There is no record of when carriers do this, unless 1 of 2 things occurs. The carrier self-reports the infraction, like you going to your local police department and telling them they missed you speeding, and you were there to turn yourself in, or… they are reported by someone who knows and understands what occurred. (Interestingly enough… if those duties were not performed, then those timelines have not even started…)

- Final Demands, Engineer rebuttals. All crucial, regardless of whether it changes the carriers’ mind or not. It is closing the claim out, and leaving a blueprint of what occurred, and what needs to occur to reach indemnity.

So the question is… what type of “Blueprint” will you leave?

Let’s uphold professionalism and protect the insured—together.

Statute, Policy, Facts of the loss, the Tripod of any claim. All factual. Crazy part... the moment I understood this, is the moment everything changed and the "process" was completed. We are not licensed to fight... attorneys are.

We are licensed to "Perform the Duties After a Loss for an insured..." That's it. Nothing more... by license.

What's the answer Cal?

Process. Boring, dull... beautiful process. Then, like anything else, fitness, social media... you have to stick with it. If the process is sound, legal, and moral... Patience will be your friend. Complete your portion of the claim, or more specifically... the Insured's Duties After a loss. If the carrier participates... or not, is out of your control. Having an answer for when they do not is not, and should never be. I believe it is our duty.

We teach that process.

Cal Spoon

{kind=link}